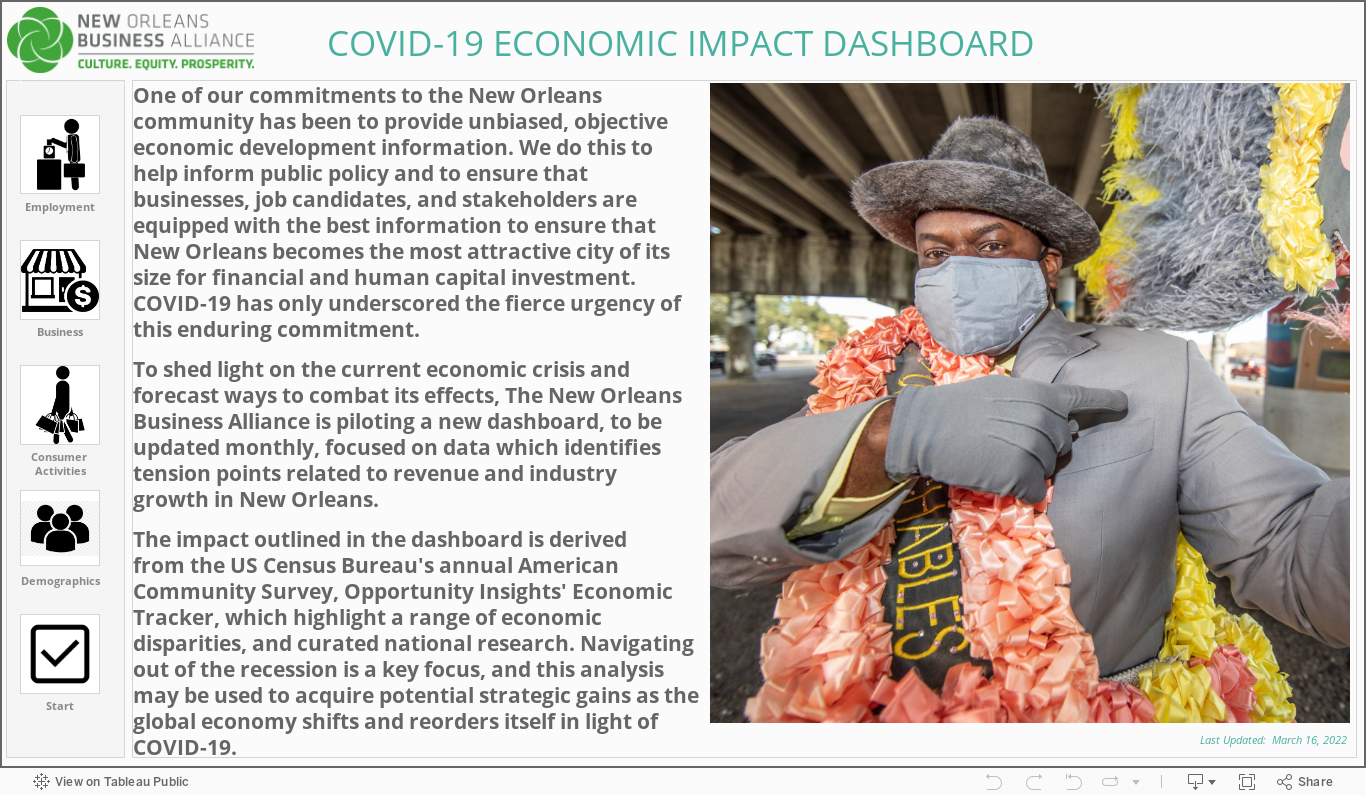

Tracking the

Economic Impacts of COVID-19

A few considerations while reviewing the dashboard:

- The purpose of this tool is not data analysis, but data accessibility for forecasting the impact of COVID-19 with interactive features.

- This dashboard is a work in progress focused on providing time-sensitive data in an interactive format, NOLABA intends to update data and validate it as we learn more about the economic impact of COVID-19.

- Publicly accessible data has a lag time, meaning that the effects of COVID-19 may not show in much of the economic data sets traditionally tracked; it may take several months to fully understand the scale of the impact. As a result, we used job postings data to show near-real-time impact on the labor market of the City of New Orleans.

- The data shown is the most recent data provided and pulled from publicly accessible sources. Given the lag time of publicly accessible data, the data provided in this tool may have a lag in timeframe and vary by measurement.

Lastly, we want to acknowledge the efforts of our AVP, Data Analytics and Performance Management, Omar Stanton, in leading this effort. Lastly, we appreciate the input of Joe M. Ricks, Jr., PhD (Xavier University of Louisiana) and Robert Habans, PhD (The Data Center) in helping to refine this first edition alongside our team.

Sources

Chetty, Friedman, Hendren, Stepner, and the OI Team (2020)

Deloitte Insights: United States Economic Forecast, 2nd Quarter 2020

EMSI, Q2, 2020 Data Set: Emsi Job Postings (Louisiana Department of Labor)

https://tracktherecovery.org/

https://www.mckinsey.com/featured-insights/americas/which-small-businesses-are-most-vulnerable-to-covid-19-and-when

Sign up for our newsletter to keep up with the latest events, opportunities, and announcements from NOLABA and the New Orleans business community.